When that late-night call comes in, most families aren't thinking in legal terms. They're thinking, "How do I get my person home?" Then someone says the bond may need collateral, and the panic gets worse. People often hear that word and picture losing the family house by morning.

Take a breath. Bail bond collateral doesn't automatically mean you're handing over everything you own, and it doesn't mean every bond will require the same kind of security. In many Colorado cases, the question is more practical: Is collateral necessary here, or can a strong cosigner and the right paperwork be enough?

That answer depends on the bond amount, the risk the bail company is taking, the defendant's history, and what kind of asset or financial backing is available. Families usually need help sorting through three decisions fast. First, whether they need collateral at all. Second, whether a cosigner is strong enough on their own. Third, if collateral is needed, which asset creates the least risk for the family.

That Phone Call What Happens When Bail Requires Collateral

A mother calls after midnight. Her son is in jail. She has the bail amount written on a notepad, she's repeating the charge to herself so she doesn't forget it, and she keeps asking the same question: "What do I need to do right now?"

Then she hears a new phrase. "You may need collateral."

That moment feels bigger than it is. Most families hear "collateral" and think it means the bail company wants to take their property. What it really means is that the company may need a form of backup security before it posts the bond. It's part of how some bonds are approved, especially when the financial risk is higher.

What families usually need first

Before you worry about deeds, titles, or signatures, get the basics straight:

- Confirm the jail and booking details: Make sure you have the correct facility, the person's full legal name, and the case information if available.

- Ask what type of bond was set: Some bonds can be handled through a surety bond. Others may have different court requirements.

- Find out whether release can start remotely: Many families don't need to sit for hours at a detention center if documents can be handled electronically.

- Get a simple explanation of next steps: A good agent should tell you what to gather, what can wait, and what decision matters most now.

If you're still trying to get your bearings, this guide on how to get out of jail gives a clear overview of the release process.

Practical rule: Don't make decisions about your house, car, or savings until someone has explained whether collateral is actually required for this bond.

Why the word sounds scarier than the process

Families are under pressure, so every term feels heavy. But collateral is just one part of bail underwriting. Sometimes it's required. Sometimes it isn't. Sometimes a cosigner with strong ties to the defendant is enough. Sometimes the bond amount or risk level means the company needs property, cash, or another asset to secure its position.

The key is not to guess. Ask direct questions. Is collateral required in this case? If yes, what kind? If no, what makes the bond approvable without it? Those answers will tell you far more than the word itself.

Collateral Is Not the Fee Unpacking the Two Costs of Bail

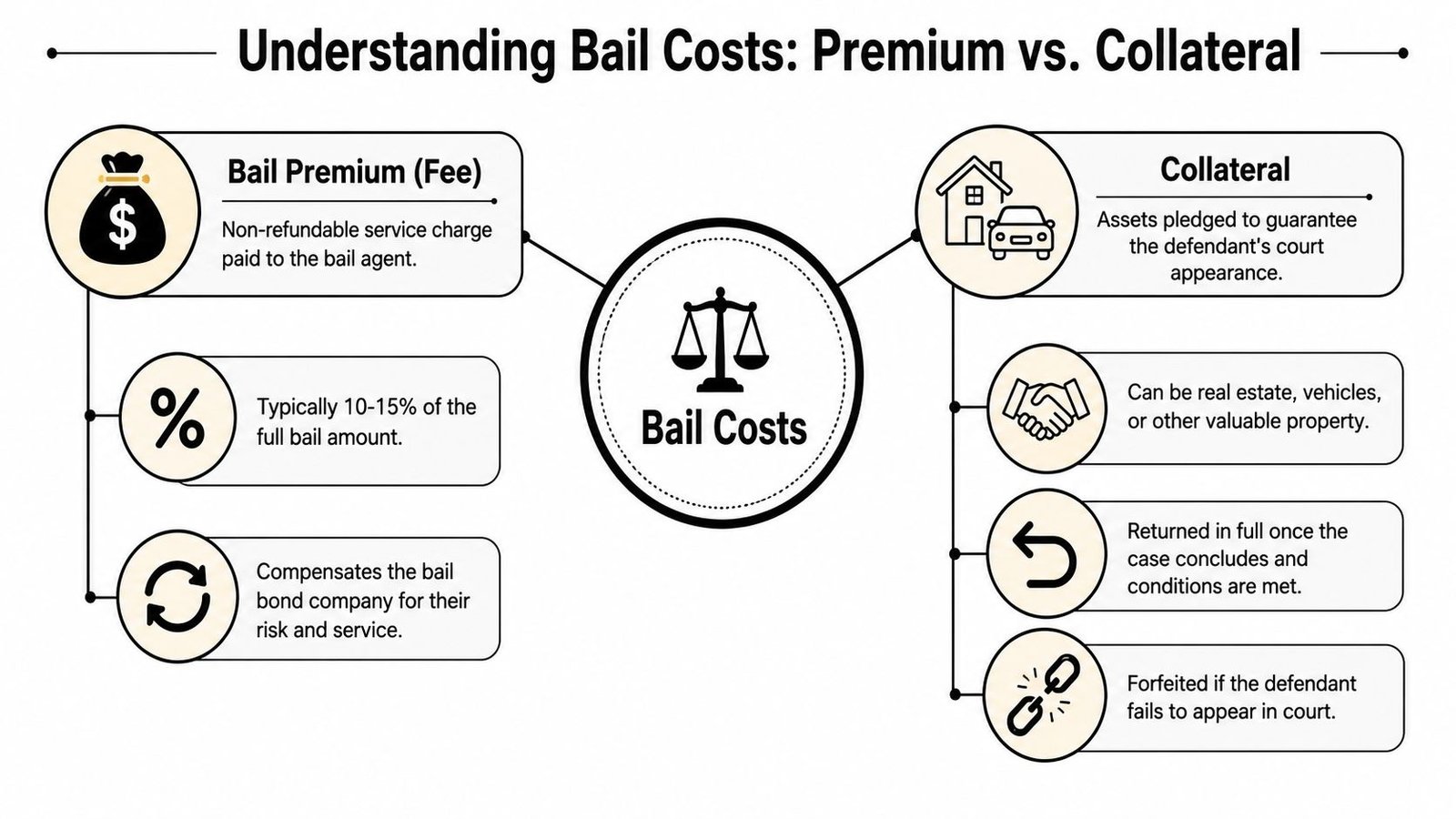

A lot of Colorado families get stuck on the same question during that first call: "If I can pay the bond fee, why are you asking about my car or house too?" The short answer is that you may be dealing with two separate parts of the same release.

One part is the fee, often called the premium. That is the charge for the bail bond service, and it is generally not refunded once the bond is written. The other part is collateral, which is security the company may ask for if the risk is higher. If the defendant follows the court's rules and the bond is discharged properly, the collateral is released back to you.

A simple way to separate them is this: the fee pays for the bond company to post the bond. Collateral protects the company if the defendant does not appear and the bond is forfeited.

That difference matters because collateral is not automatic in every case. Sometimes a strong cosigner is enough. If the cosigner has stable income, solid local ties, and a clear ability to keep the defendant on track for court, the bond may be approved with the fee and no pledged asset. In other cases, the bond amount, the charge history, prior failures to appear, or weak financial backing can lead the agent to ask for collateral.

Families often feel a wave of panic at that point, especially if the word "collateral" makes it sound like the company is taking the asset. Usually, that is not what is happening. The asset is being pledged as security, much like a backstop. One explainer makes the same distinction clearly in this discussion of collateral versus bail bond payment.

The practical question is not just "Do we have something to pledge?" It is "Should we pledge this particular asset, or do we have a safer option?"

For example, a family home may have enough equity to satisfy the bond company, but that does not always make it the best first choice. A vehicle with clear title, a savings account, or another asset with easier paperwork may expose the family to less stress. If the asset is jewelry or precious metals, getting a realistic value matters before you offer it. Carat 24's guide to understanding gold value can help you see how valuation works before you bring that option to an agent.

Here are the questions that usually lead to a better decision:

- Can this bond be approved with a strong cosigner and the fee alone?

- If not, what is the smallest amount of collateral that will work?

- Is a house really necessary, or would a vehicle or cash security be enough?

- What paperwork will the agent need to verify ownership and value?

- What exactly must happen for the collateral to be released at the end?

Those questions keep you from overcommitting. They also help you compare your options calmly instead of pledging the biggest asset you own out of fear.

If you want more context on why bond companies separate the service charge from the security, this explanation of how bondsmen make money lays out the business side in plain language.

Acceptable Bail Bond Collateral in Colorado

A Colorado family usually asks this question right after the fee discussion: "Do we have to put up property, or can a cosigner be enough?"

The answer depends on risk. Some bonds are approved with a reliable cosigner and the premium payment alone. Others require added security because the bail amount is higher, the case has more risk factors, or the person signing for the defendant does not have enough financial strength on paper. The ultimate decision is not just what you own. It is which option solves the problem with the least risk to your family.

Collateral works like a safety deposit for the bond company. The company is looking for something it can confirm, estimate, and document if the defendant misses court and the bond is forfeited. That is why the same asset can be accepted in one case and rejected in another.

What usually makes collateral acceptable

Three things usually matter most:

- Clear ownership: The person offering the asset can show it belongs to them.

- Documented value: The asset has records that support a realistic value.

- A usable legal paper trail: The company can document its interest in the asset if needed.

That is why homes, land, and vehicles come up often. They usually have deeds, titles, loan records, and other paperwork an agent can review without guessing.

Common Collateral Types Accepted in Colorado

| Asset Type | Commonly Accepted? | Key Requirement |

|---|---|---|

| Real estate | Often yes | Clear ownership, available equity, and property documents |

| Vehicle | Often yes | Title, registration, and enough value to matter |

| Cash | Sometimes | Immediate verification and transferability |

| Jewelry | Sometimes | Proof of ownership and support for value |

| Investment accounts or similar assets | Sometimes | Documentation showing ownership and value |

| Personal household goods | Usually no | Hard to value and hard to liquidate |

| Heavily financed vehicle | Sometimes not | Limited usable value if debt is too high |

| Signature alone | Sometimes | Depends on the cosigner's strength and overall risk |

A house is often the largest asset a family has, so it gets mentioned first. It should not be your automatic first choice.

If your goal is to get the bond approved while limiting family stress, ask a narrower question: would a smaller asset work? A vehicle with a clear title may be easier to document and less emotionally risky than tying the bond to a home. Cash or funds in an account may also be simpler in some cases. Jewelry can be an option too, but only if the value can be supported in a way the agent will accept. If you are considering gold or jewelry, Carat 24's guide to understanding gold value can help you understand how buyers and appraisers look at value before you offer that asset.

The best collateral is usually the one that meets the bond company's requirement without putting your most important asset at unnecessary risk.

When a strong cosigner can replace collateral

This is the part many families want clarified. Collateral is not always required.

A strong cosigner can sometimes be enough if the person has steady income, stable residence, reachable contact information, and a real ability to keep the defendant on track for court. An agent is asking a practical question: if this person is released, how likely is it that they will appear, and how dependable is the person signing for them?

For a lower-risk bond, a dependable cosigner may remove the need for property. For a higher-risk bond, the company may still want collateral even with a good cosigner. That is why two families can hear different answers even when the bail amount looks similar.

If you are weighing options, it also helps to understand the difference between a surety bond and a cash bond in Colorado. That comparison makes it easier to see why collateral questions show up more often with surety bonds.

How Bail Agents Use and Secure Your Collateral

When someone pledges collateral, the process should be orderly, documented, and clear. It isn't just a handshake and a promise. Bail underwriting treats collateral as a loss-mitigation mechanism. Agents look for assets with verifiable title and documented value, such as real estate or vehicles, and the bond is released only after those terms are documented and accepted, as explained in this overview of how bail bond collateral works.

Why paperwork matters so much

From the family's point of view, paperwork can feel like a delay. From the bail agent's point of view, it's what turns a vague promise into enforceable security.

For example, with a vehicle, the agent may need to review the title, registration, and proof of ownership. With real estate, the process often involves more paperwork because the ownership record, existing loans, and available equity all matter. The more liquid and easier-to-document the asset is, the smoother the approval process tends to be.

What "secured" usually means in real life

For real estate, the company may use legal documents that create a claim against the property for the bond obligation. For a vehicle, the process may involve title-related documentation. For cash or certain valuables, it may involve direct possession or a written collateral agreement describing the terms.

That doesn't mean the company is trying to take the property. It means the company needs a legal path to recover loss if the bond is forfeited.

Here is what families should expect the company to verify:

- Ownership: Who legally owns the asset

- Value support: What documents support the claimed value

- Existing debt: Whether loans or liens reduce usable value

- Transferability: Whether the asset can secure the bond in a practical way

Ask for the contract terms in plain English

Before signing anything, ask the agent to explain:

- What exactly is being pledged

- What event would put that asset at risk

- What the company will do when the case is over

- What happens if the defendant misses court but is later returned

A clean explanation should match the written agreement. If the paperwork feels hard to follow, ask questions until it doesn't. This is one reason it helps to read more about a bail bond contract before you sign.

The Step-by-Step Process of Pledging Collateral

When families are stressed, they don't need abstract theory. They need a checklist they can follow without guessing. The collateral process usually becomes manageable once you break it into a few concrete steps.

Step 1 through Step 3

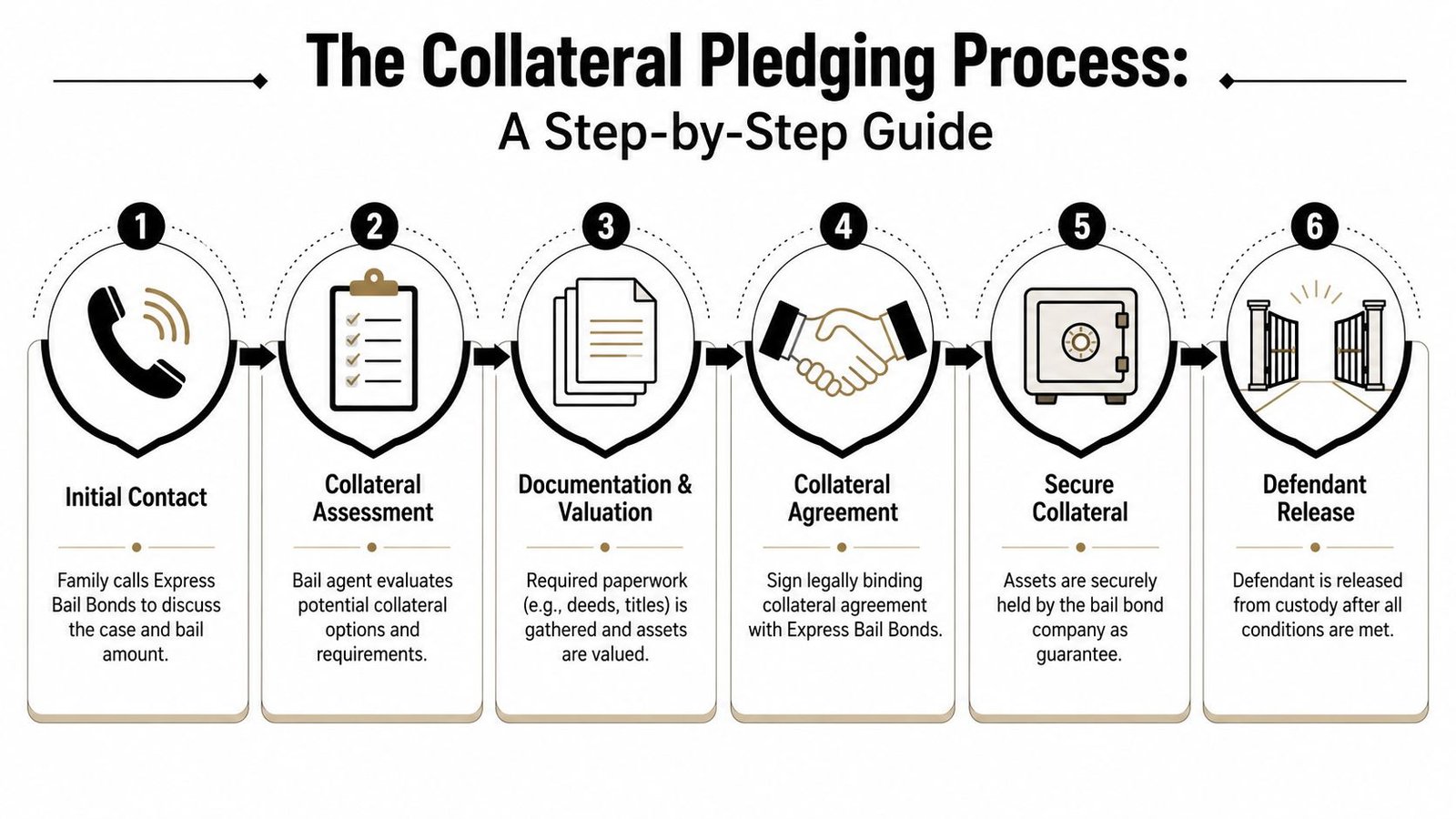

Initial contact and case review

You provide the defendant's name, jail, charges if known, and bail amount. The agent reviews the case and tells you whether the bond may be approved with a fee only, with a cosigner, or with collateral.Collateral discussion

If collateral may be needed, the conversation turns practical. What assets are available? Who owns them? Are they local? Is there a title, deed, or other paperwork ready?Document gathering

This is usually where families slow down, but it doesn't have to be complicated. Gather what supports ownership and value. For real estate, that may include deed-related records. For a vehicle, title and registration are common starting points.

A video walkthrough can help if you're more comfortable seeing the process than reading it.

Step 4 through Step 6

Application and collateral agreement

The indemnitor or cosigner completes the bond paperwork and reviews the collateral terms. This is the stage where names, obligations, and asset descriptions need to be accurate.Signing and securing the collateral

Depending on the asset, this could mean signing collateral paperwork, providing title documents, or completing property-related forms.Bond posting and release process

Once the bond is approved and posted, the jail processes the release according to its own timing and procedures.

What helps the process move faster

Families often ask what causes delay. It's usually one of these:

- Missing ownership documents

- Name mismatches on titles or deeds

- Unclear value of the asset

- Uncertainty about who is signing as indemnitor

- A defendant's release conditions that require extra review

Bring the cleanest paperwork you have. Good documents lower stress for everyone in the process.

Remote processing can make a big difference for out-of-county or out-of-state family members. Much of the delay people fear comes from assuming every signature has to happen in person. In many situations, a large part of the paperwork can be handled electronically, which is a major relief when you're trying to coordinate from work, home, or another county.

Risks vs Rewards Reclaiming Your Assets After the Case

Once collateral is pledged, families usually focus on one question: "How do we make sure we get it back?"

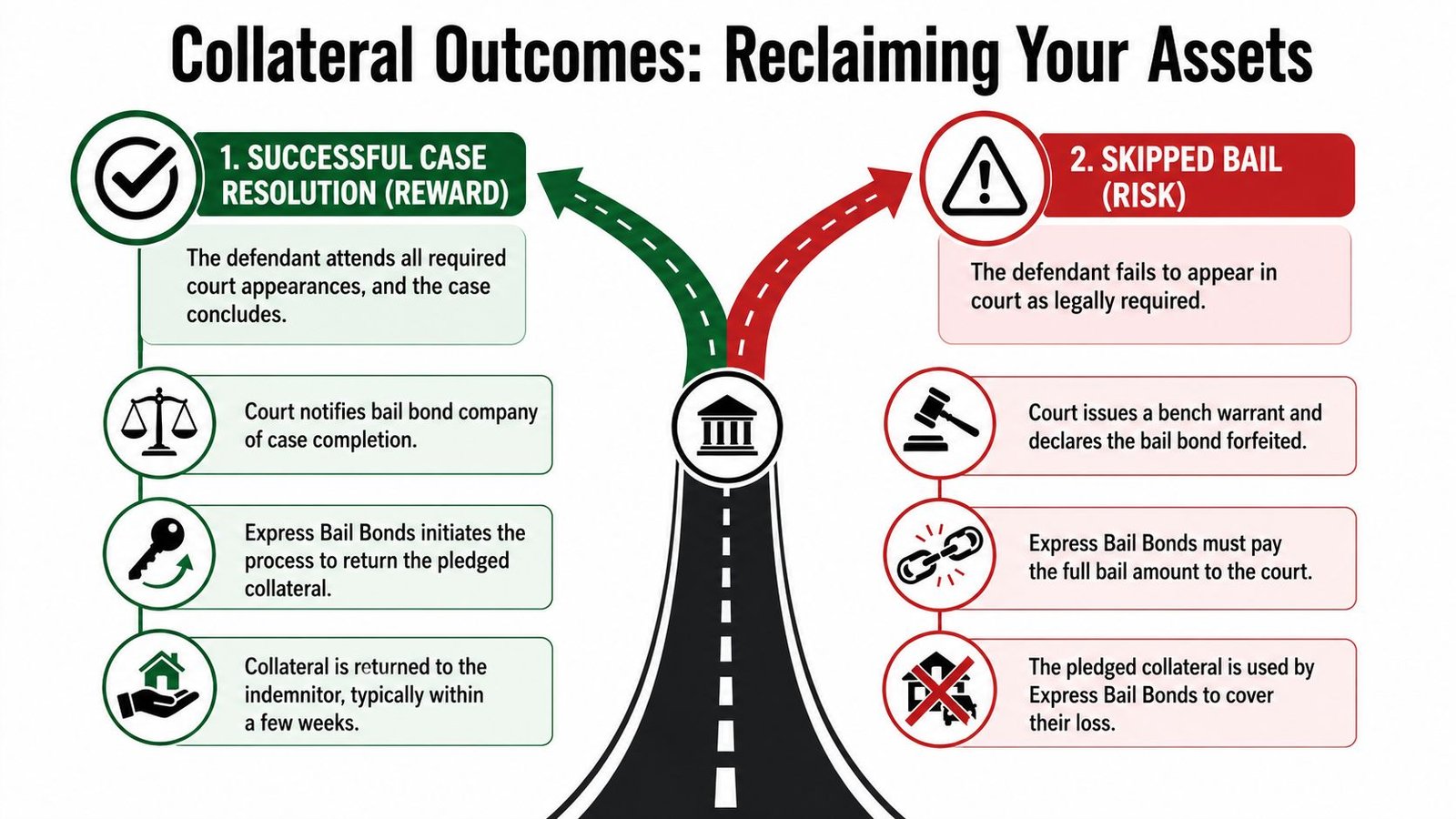

The answer turns on one issue above everything else. Does the defendant appear as required? Collateral has a default-contingent enforcement role. If the defendant appears at all hearings, the collateral is returned when the case ends. If the defendant fails to appear, the surety may seize and sell the asset to recover losses, which makes the arrangement economically similar to secured lending, as described in this explanation of collateral and forfeiture consequences.

Path one shows up and finishes the case

This is the outcome every family wants. The defendant attends required court appearances, follows release conditions, and the case reaches a point where the bond obligation ends.

When that happens, the company starts the release process for the collateral. The exact mechanics depend on what was pledged. A title may be returned. A property-related claim may be released. The key point is that collateral is not supposed to sit in limbo forever once the bond has been properly exonerated.

What families should do on this path:

- Keep records of the case status

- Save copies of the collateral agreement

- Ask what proof of case completion the company needs

- Follow up until the release paperwork is complete

Path two misses court and creates exposure

Here, collateral takes on critical importance. If the defendant fails to appear, the court can move toward forfeiture and the financial risk lands squarely on the bond.

That doesn't always mean property is taken immediately. There may be efforts to locate or surrender the defendant, and the legal process has its own steps. But families should not downplay what is at stake. If the bond loss becomes final, the pledged asset may be used to cover that loss.

How to weigh house versus another asset

This is often the hardest family decision. A home may be the strongest asset available, but it's also emotionally and financially the heaviest one to place at risk.

A better question than "What can we use?" is "What can we afford to put at risk if everything goes wrong?" Sometimes the answer is a vehicle, cash, or another asset that would hurt less than the family home. Sometimes there is no practical substitute. But the decision should be made with open eyes.

If you're nervous about pledging your house, that instinct is healthy. It means you're taking the obligation seriously.

If you need to understand the court side of what happens when a defendant doesn't appear, this page on what bond forfeiture means is worth reading before you sign.

Frequently Asked Questions for Colorado Families

Your phone rings late at night. A relative has been arrested. Someone says, "We may need collateral," and suddenly your mind jumps to your house, your car, your savings, and everything that could go wrong.

That reaction is normal.

Families usually need answers in plain language, not legal jargon. Bail bonds are also part of a large national business. According to IBISWorld's bail bond services industry research, the U.S. bail bond services industry was projected to reach $3.5 billion in revenue in 2026, with 20,886 businesses operating in 2025 and industry size growing at a 3.3% CAGR from 2020 to 2025. One reason collateral comes up so often is simple. Bail companies have to measure risk in a consistent way.

Can I get a bail bond without collateral

Yes. In some Colorado cases, a bond can be written with a strong cosigner and no pledged property.

A good way to look at it is this. Collateral is a backup plan for the bond company. If the case, bond amount, and defendant's history suggest lower risk, a qualified cosigner may be enough on its own. If the risk looks higher, the company may ask for an asset as added security.

So ask the question directly: "Can this bond be approved with a cosigner alone, or is collateral required?"

When is a strong cosigner enough

A strong cosigner is someone the bond company can reasonably rely on. That usually means a close relationship with the defendant, steady employment or income, stable contact information, and a willingness to stay involved until the case is over.

A cosigner works a bit like a co-borrower on a loan. The company is asking, "If problems start, will this person answer the phone, help keep the defendant on track, and take the obligation seriously?" A parent, spouse, sibling, or long-term partner often carries more weight than someone who barely sees the defendant.

If you are the cosigner, expect questions. That is not a bad sign. It usually means the company is deciding whether your strength as a signer can reduce or replace the need for collateral.

Should I use my house if another asset is available

Start with the risk, not the asset.

Your house may have enough value to satisfy the collateral requirement, but it is also the asset families feel most strongly about, for good reason. If something less painful can cover the same need, many families sleep better choosing that option.

A vehicle title, cash, savings, or another asset may be easier to pledge because the downside is more limited. The tradeoff is that those assets may not have enough value for the bond amount. The right question is: "If the worst-case outcome happened, which asset would do the least long-term harm to our family?"

What if the property is in another Colorado county

That can still work. The county where the property sits does not always control whether it can be used as collateral.

What matters more is clear ownership, enough value, and documents the bail company can verify. If the paperwork is in order, property in another Colorado county may still be acceptable.

How long does it take to get collateral back

It depends on two things. First, the case has to reach the point where the bond obligation is over. Second, the release paperwork has to be completed correctly.

Some assets are easier to release than others. A vehicle title may be returned faster than a property-related filing that requires recorded documents. Keep copies of everything you sign, and ask early what proof of case completion the company will need from you.

What rights do I have as a cosigner if I think the defendant won't appear

Speak up right away.

If you believe the defendant is talking about skipping court, leaving town, or cutting off contact, call the bond company immediately. A cosigner is not stuck waiting for disaster. Early notice gives the company more options to address the problem before it becomes a bond loss.

Silence helps no one. Fast communication gives your family the best chance to limit damage.

What should I ask before signing

Keep your questions practical:

- Is collateral required, or can a strong cosigner qualify for this bond

- Why is the company asking for collateral in this case

- What asset would the company accept besides a house

- How much value does the asset need to have

- What specific event puts the collateral at risk

- What documents will I receive showing the collateral was released

- Who should I contact immediately if the defendant starts talking about missing court

Where should I start if everything feels overwhelming

Start small. Get the full name of the defendant, the jail location, the bond amount, and the charges if you have them. Then ask one of the most important questions first: "Do we need collateral here, or is a strong cosigner enough?"

That single answer often clarifies the whole decision. If collateral is required, compare your options carefully before offering your house. If it is not required, you may be able to move forward with less risk than you feared.