A secure bond means the court requires a financial guarantee before release, usually cash, property, or other collateral. If property is used, some jurisdictions require 1.5 times the bond amount in clear equity, so a $20,000 bond would need at least $30,000 in unencumbered equity.

If you're looking this up, you're probably dealing with a call from jail, a court date you didn't expect, and a lot of words that all sound the same. Secure bond. Surety bond. Cash bond. Unsecured bond. In the moment, the primary question isn't legal theory. It's simple: What does this mean for me right now, and how do I help get someone out?

The short answer is that a secure bond means release isn't based on trust alone. The court wants something of value standing behind the promise to appear. That can affect how fast the person gets out, what paperwork you'll need, whether you need a cosigner, and whether your home, car, or cash is part of the process.

What Is a Secure Bond and Why It Matters Now

A secure bond is a bail arrangement backed by something of value. That backing can be cash, property, or other collateral, which gives the court or bonding party a financial guarantee that the defendant will show up for every required hearing. If the person misses court, the pledged security can be at risk.

That sounds technical, but the practical meaning is immediate. If the judge set a secure bond, your loved one usually can't walk out by signing a promise alone. Someone has to satisfy that financial condition first.

What this means in plain English

The court is saying, "We will allow release, but only if someone puts real value on the line."

That value can take different forms:

- Cash to the court when the court accepts a cash-backed release

- Property equity when real estate is used to secure the bond

- A surety arrangement when a bail bondsman guarantees the bond and may require collateral or a cosigner

Practical rule: The bond type matters as much as the amount. Two people can have the same bond amount and face very different release steps depending on whether the bond is secured, cash-only, or surety-eligible.

The idea itself isn't new. The history of surety bonding goes back to the Old Testament, and the modern bail bond business model developed in the early 1800s. Washington state legislative materials also note that the standard premium historically became 10% of the bail amount, paid up front and typically non-refundable, with collateral sometimes required for the full bond value, as explained in this Washington legislative document on surety bonding history.

If you're trying to make sense of how a bondsman fits into all this in Colorado, this guide on what a surety bail bond is and how it works in Colorado breaks down the process in everyday terms.

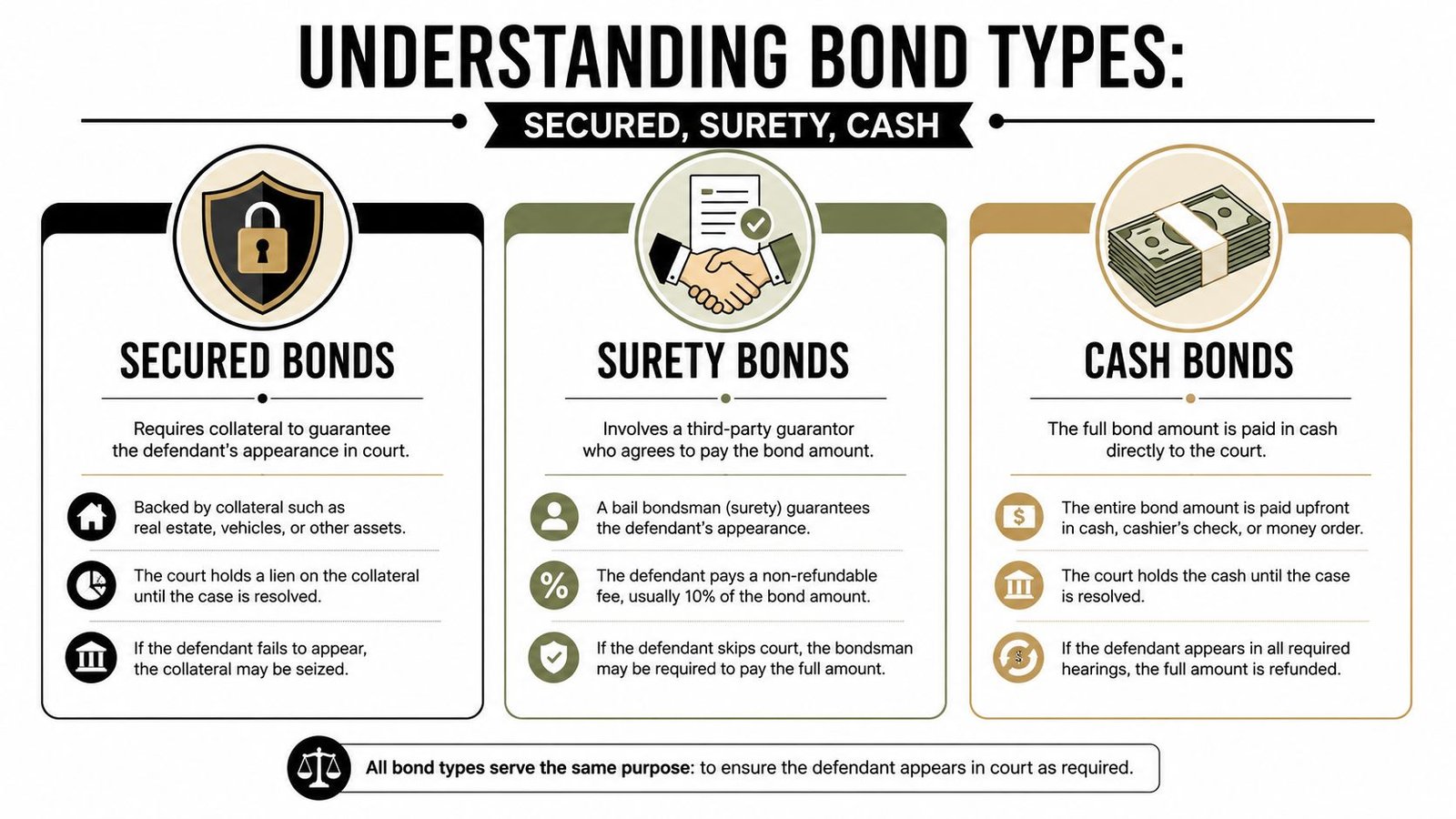

Secured vs Surety vs Cash Bonds Explained

Your loved one calls from jail and says, "My bond is set." The next question is the one that affects your next hour, not just your understanding of legal terms. Do you need the full amount in cash, can a bondsman post it, or is the bond tied to property or other security?

People often use these terms as if they mean the same thing. They do not. In real life, the difference decides whether you can act tonight, whether you need a cosigner, and whether a house, car, or cash may be at risk.

A simple way to sort it out is to treat each bond type like a different way of giving the court confidence that the defendant will come back.

Cash bond

A cash bond usually means the full bond amount must be paid directly to the court before release. The court holds that money while the case is open, subject to its rules and the defendant's compliance.

For a family in Colorado, this usually creates one immediate question. Can we get the full amount together fast enough? If the bond is high, or if it is late at night or over a weekend, that can be the hardest path because the court wants the whole amount, not part of it.

Surety bond

A surety bond uses a third party, usually a bail bondsman, to guarantee the bond to the court. Instead of paying the full bond amount to the court, the family pays a premium, signs an agreement, and may need a cosigner or collateral depending on the case.

That changes the practical decision. If the bond is surety-eligible, you may be able to start the release process without producing the full face amount in cash. For a closer side-by-side explanation, this comparison of surety bond vs cash bond helps clarify what each option requires.

Secured bond

A secured bond describes the backing behind the release. It means the bond is supported by something of real value, such as cash, property, or another asset, rather than an unsecured promise to appear.

That is the part families usually feel right away. If the court or bond arrangement requires security, the conversation shifts from "How much is the bond?" to "What do we have to put on the line?" A secured bond can involve cash posted to the court, or it can involve a surety bond that is itself backed by collateral.

So these terms can overlap. A cash bond can be a form of secured bond because cash is the security. A surety bond can also involve a secured arrangement if the bondsman requires collateral. The label tells you what kind of backing the court or bonding company expects.

A quick comparison

| Bond type | What usually backs it | What it means for you right now |

|---|---|---|

| Cash bond | Full cash amount paid to the court | You need the full amount available before release |

| Surety bond | A bondsman guarantee, often with a premium and signed agreement | You may be able to post bond without paying the full amount to the court |

| Secured bond | Cash, property, or another pledged asset | You need to know what asset or guarantee must be put at risk |

If you only ask one question, ask this one: Is the bond cash-only, surety-eligible, or secured by specific collateral? That answer usually tells you your next step in Colorado faster than the bond amount alone.

The Role of Collateral and Cosigners

When families hear "secure bond," what they usually want to know is whether they'll need to put up property and whether signing for someone puts their own finances at risk. The answer is often yes. That's why it's important to slow down and understand what you're agreeing to.

What counts as collateral

Collateral is something of value pledged to reduce the risk of non-appearance. Depending on the bond arrangement, that might include:

- Real property such as a house with usable equity

- Vehicles where title can be pledged

- Cash or other valuable assets that can stand behind the bond obligation

Some jurisdictions require the equity in real property to be well above the face amount of the bond. Virginia's commission highlights a 1.5× equity requirement in some settings, meaning a $20,000 bond would need at least $30,000 in unencumbered equity, as noted in Virginia's secured bond study highlights.

That doesn't mean every Colorado case follows that exact formula. It does show why families are sometimes surprised when a house can't be used as easily as they expected. Equity has to be real, clear, and sufficient.

If you need a practical overview of what agencies may accept and how the process works, this page on bail bond collateral gives a plain-language starting point.

What a cosigner is really agreeing to

A cosigner isn't just helping with paperwork. A cosigner is taking financial responsibility for the defendant's compliance with the bond terms.

That usually means the cosigner is agreeing to:

- Back the bond obligation if the defendant doesn't follow court requirements

- Provide truthful information during the bond process

- Stay involved after release by helping make sure the defendant gets to court

A cosigner should never sign because they're feeling pressured in the hallway or over the phone. Sign only after you understand what property, money, or legal responsibility is attached to your name.

The premium question families always ask

Another common point of confusion is the premium paid to a bail bond company. Historically, surety materials cited by Washington state note an industry-standard premium of 10%, paid up front and typically non-refundable, as described earlier in the article. The key idea for families is simpler than the history lesson. The premium is different from collateral.

Collateral is security against loss.

The premium is the fee for writing the bond.

Those are two separate things, and people often mix them together during a stressful release.

Why a Judge Might Require a Secure Bond

When a judge sets a secure bond, families often hear it as a judgment on the person. That's usually not the most useful way to look at it. The court is making a release decision based on risk, court appearance concerns, and the facts in front of the judge.

The difference from an unsecured bond

The biggest practical difference is timing and money. A secured bond requires cash or collateral upfront. An unsecured bond is a promise to pay later if the defendant fails to appear. Neutral legal explainers also note that judges usually reserve unsecured bonds for lower-risk defendants with little or no criminal history, as explained in this overview of different types of bail bonds.

That means when a judge chooses a secured option, the court is usually asking for more assurance before release happens.

Factors families should keep in mind

No two hearings are exactly alike, and local practice matters. But these are the kinds of issues that often affect whether a judge is comfortable with a less restrictive release:

- Community ties such as stable housing, family connections, or local employment

- Criminal history especially if the person has prior cases or prior failures to appear

- Case seriousness because more serious charges can lead to tighter release conditions

- Flight risk concerns if the court thinks the person may not return

If you want a clearer picture of what happens when the judge first addresses release conditions, this guide to what happens at a bail hearing can help you understand the setting.

When a judge requires a secure bond, the family usually gets farther by focusing on compliance and logistics than by arguing over the wording. The immediate question becomes what form of security the court will accept and how quickly you can provide it.

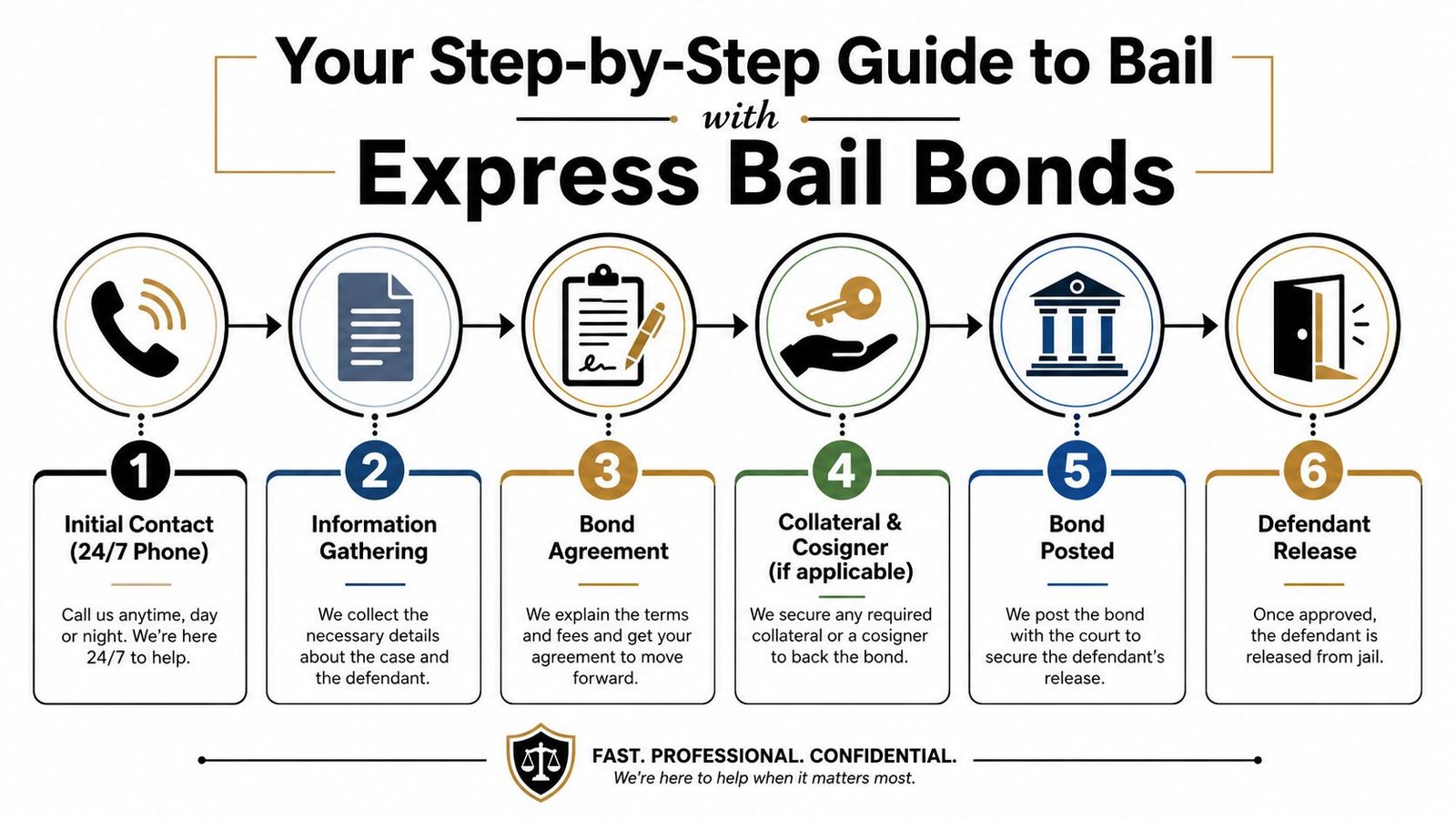

Posting Bond in Colorado with Express Bail Bonds

Once the bond is set, the process becomes practical fast. You need names, booking details, the jail location, the bond amount, the bond type, and a clear sense of whether the court allows a surety bond or requires something else.

This visual helps show the typical flow from first contact to release.

Step one through step three

Start by gathering the basics before you call anyone:

- Defendant information. Full name and date of birth if you have it.

- Jail or detention facility. The county matters because procedures differ.

- Bond terms. You need the amount and whether the bond is surety-eligible, secured, or cash-only.

From there, a bail agency can tell you whether the bond can be posted through a bondsman and what documents may be needed. If you want to prepare ahead, the bail bond application shows the kind of information agencies commonly request.

One option families use is Express Bail Bonds, a Colorado bail bond agency that handles surety bonds and electronic paperwork for many situations statewide. If the arrest happened in Jefferson County, the local detention process may involve details covered on their Jefferson County Golden bail bond page. For Arapahoe County matters, their Centennial bail bonds page focuses on that area.

Why release time often takes longer than expected

Families often think posting the bond and walking out happen back to back. Sometimes they do. Often they don't.

A bondsman may process paperwork in as little as 15 minutes, but actual release from some Colorado jurisdictions can still take a few hours to over 16 hours after the bond is posted, depending on staffing and facility procedures, as explained in North Main Bail's Colorado release timing FAQ.

Don't measure the timeline only by when the bond gets posted. Measure it by when the jail completes its own release steps.

That delay can come from internal jail workflow, shift changes, warrant checks, property return, or release queue issues. So if you're arranging a ride, child care, or work coverage, plan for uncertainty.

A short video can also help if this is your first time dealing with bail:

A practical Colorado checklist

Before you commit, ask these questions clearly:

- What bond type is allowed so you know whether a surety bond is even an option

- Who must sign because some cases require a financially responsible cosigner

- Whether collateral is required and what form the agency will review

- What the jail's release routine looks like so you don't expect an instant release

If you're calling from out of state or trying to do this from home, electronic signatures and remote document handling can make the process easier. The key is getting accurate information from the jail and moving in the order the facility and court require.

Common Questions About Secure Bonds in Colorado

A lot of families ask the same thing after release. "Now what am I still responsible for?" That is the right question, because a secure bond can keep affecting you until the case ends.

What happens to the collateral after the case is over

Collateral is usually returned once the bond obligation is finished and the terms of the bond agreement have been met. In plain terms, the collateral was there as a safety net. It was not meant to become a permanent payment if the case was handled correctly.

The timing depends on who is holding it and what was pledged. Cash may be released through one process. A vehicle title or property paperwork may take another. Before you sign, ask for the release steps in writing so you know what documents you will need later and who authorizes the return.

What are my responsibilities as a cosigner after release

Your job as a cosigner continues after the person gets out of jail. You are the financially responsible party on the bond, so you should stay in contact, track court dates, and make sure the defendant knows every appearance matters.

That does not mean you run the criminal case. It means your name, money, or property may be on the line if the bond terms are broken.

What happens if the defendant misses a court date

This is the part families worry about most, and for good reason. If the defendant misses court, the court can treat that as a bond default, and the security behind the bond may be at risk.

For you, that can mean losing the cash you posted or facing a claim against the collateral you pledged, such as a vehicle title or an interest in property, depending on the agreement and the case. As noted earlier, a secured bond is backed by something of value. If court appearances are missed, that backing can be forfeited.

The safest approach is simple. Treat every court date as mandatory unless the court changes it.

Can I get a bond for someone in any Colorado jail

Sometimes yes, sometimes no. It depends on the judge's order, the bond type, and the jail's process.

A person may be in a Colorado jail, but that does not automatically mean a bondsman can post the bond. Some bonds are cash-only. Some allow a surety bond. Some include holds or conditions that delay release even after the bond is handled. The practical first step is to confirm the exact bond type ordered by the court, then ask whether a licensed Colorado bail agency can post that specific bond.

A lot of confusion starts when families focus on the money before they confirm the bond type. Start with the order itself. Once you know what the judge required, your next steps become much clearer.

If you need help sorting out what a secure bond means in your case, Express Bail Bonds can explain whether the bond is surety-eligible, what paperwork may be required, and what usually affects release timing in Colorado.