You're probably here because something landed on your desk fast. A court clerk said a bond is required. A licensing form won't move without one. A contractor registration renewal is suddenly tied to bonding. Or a family member heard the word “bond” after an arrest and now everyone's talking past each other.

That confusion is normal. The word bond gets used for different situations, and people often assume it means insurance or a cash deposit. In New Jersey, it can mean something very different. The key is to slow it down and separate the moving parts so you know who is protected, who signs, and who ultimately pays if things go wrong.

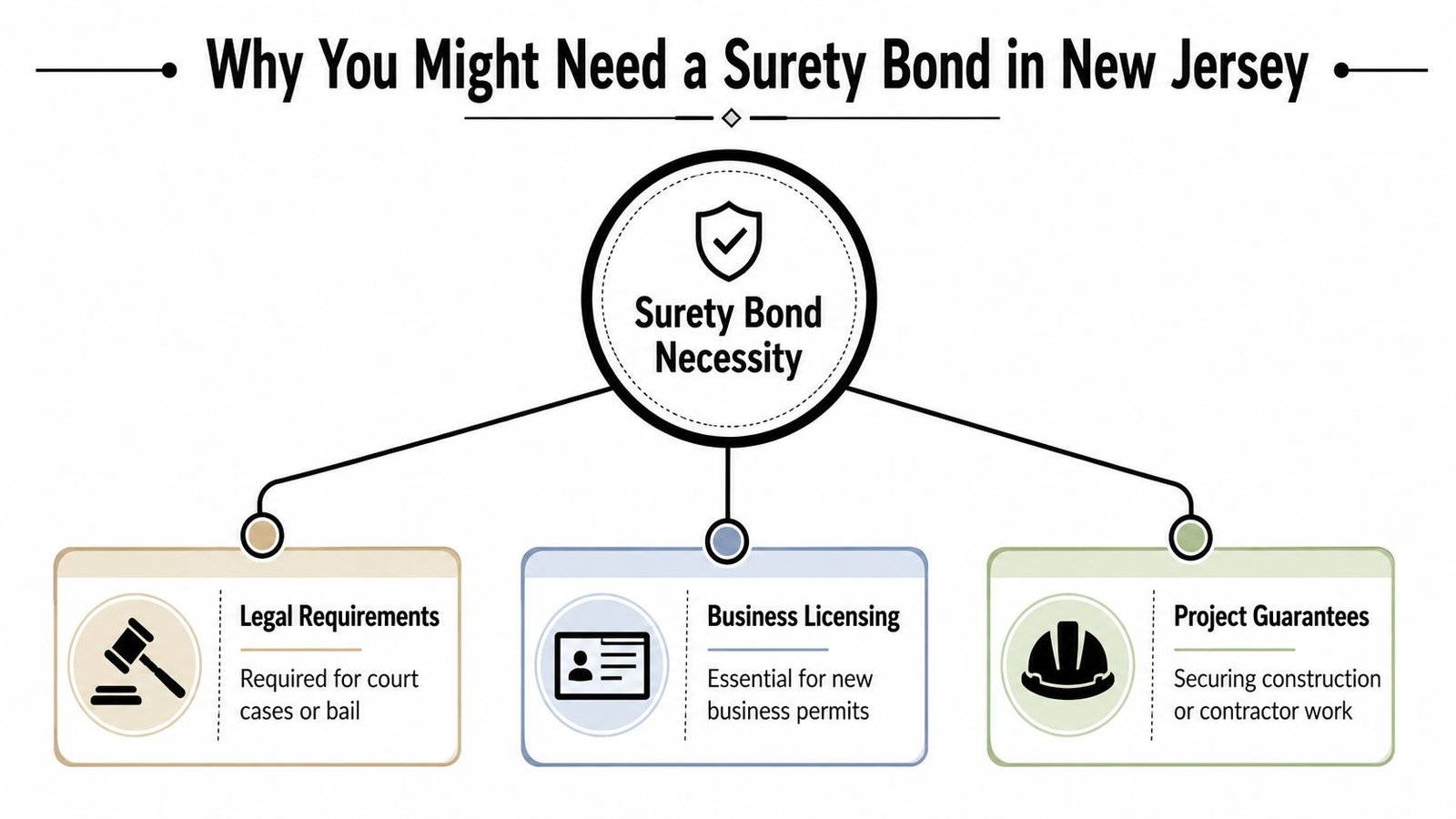

Why You Might Need a Surety Bond in New Jersey

A surety bond is easiest to understand if you think of it as a professional cosigner arrangement. There are three parties involved. The principal is the person or business getting the bond. The obligee is the court, agency, or project owner requiring it. The surety is the company that backs the promise.

If the principal fails to do what they promised, the surety may step in and pay a valid claim. That's why bonds show up in stressful moments and formal transactions. Someone with authority wants a financial guarantee before they move forward.

Three common reasons people need one

- Legal matters: A bond may be required in a court-related situation, including bail or certain civil court matters.

- Business licensing: A state agency may require a bond before it grants or renews a license or registration.

- Construction work: A public or private project owner may require a bond before awarding work.

That's why the phrase surety bonds New Jersey covers more ground than commonly expected. It isn't one product. It's a category of financial guarantees used in very different settings.

Where people get tripped up

Many people hear “bond” and assume the money works like insurance. Others assume the bond amount is the same thing as the upfront cost. Neither assumption is always right. The bond amount is the guarantee required by the obligee. The amount you pay to obtain the bond is usually a separate premium or fee.

Practical rule: Before you sign anything, ask three plain questions. Who requires the bond, what promise is being guaranteed, and who pays if a claim is made?

If you want a plain-English overview of bond basics, this short guide on what a surety bond is helps clear up the vocabulary. For a broader look at state-specific options, Liberty Insurance Associates surety bonds is also a useful reference point when you're trying to match the bond type to the obligation.

The Main Types of New Jersey Surety Bonds

The cleanest way to sort this out is by purpose. In New Jersey, most bond questions fall into one of three buckets. Court and bail bonds, contract bonds, and commercial bonds.

Court and bail bonds

This is the category families usually know first. A bail bond helps guarantee that a defendant appears in court as required. In practical terms, it gives the court a financial backstop tied to the defendant's release conditions.

That's why people often compare a surety bond with posting cash directly. They are not the same tool, and this side-by-side explanation of surety bond vs cash bond makes that difference easier to understand when the pressure is high.

Court bonds can also come up outside criminal cases. Some are tied to appeals, fiduciary duties, or property disputes. The common thread is simple. The court wants a reliable financial promise before allowing a person to move ahead.

Contract bonds

Contract bonds show up heavily in construction and public work. The two names you'll hear most are performance bonds and payment bonds. A performance bond backs the contractor's promise to complete the work as agreed. A payment bond helps protect subcontractors and suppliers.

In New Jersey, this isn't a niche requirement. As of 2025, New Jersey mandates that contractors on public works projects over $850,000 must secure payment and performance bonds. In total, $3.7 billion in surety bond coverage supports 445 state projects, showing their critical role in protecting taxpayer funds according to New Jersey approved surety company guidance.

That tells you two things right away. First, public owners take bond backing seriously. Second, contract bonding isn't just paperwork. It's part of how the state protects jobs, vendors, and public money.

Commercial bonds

Commercial bonds usually support a license, permit, or registration. They're common in regulated industries because the agency wants proof that the business will follow the rules and handle money or obligations properly.

A few New Jersey examples make that more concrete:

| Bond type | Why it's required |

|---|---|

| Contractor compliance bond | Supports registration and consumer protection requirements |

| Auto dealer bond | Backs compliance tied to dealer licensing |

| Freight broker bond | Required for brokers operating under federal rules |

| Electrical contractor bond | Required as part of state licensure |

A commercial bond doesn't mean the business is bad or risky. It usually means the state or regulator wants a formal guarantee in place before letting the business operate.

A bond requirement often means, “You can work, but only if someone financially credible stands behind your promise.”

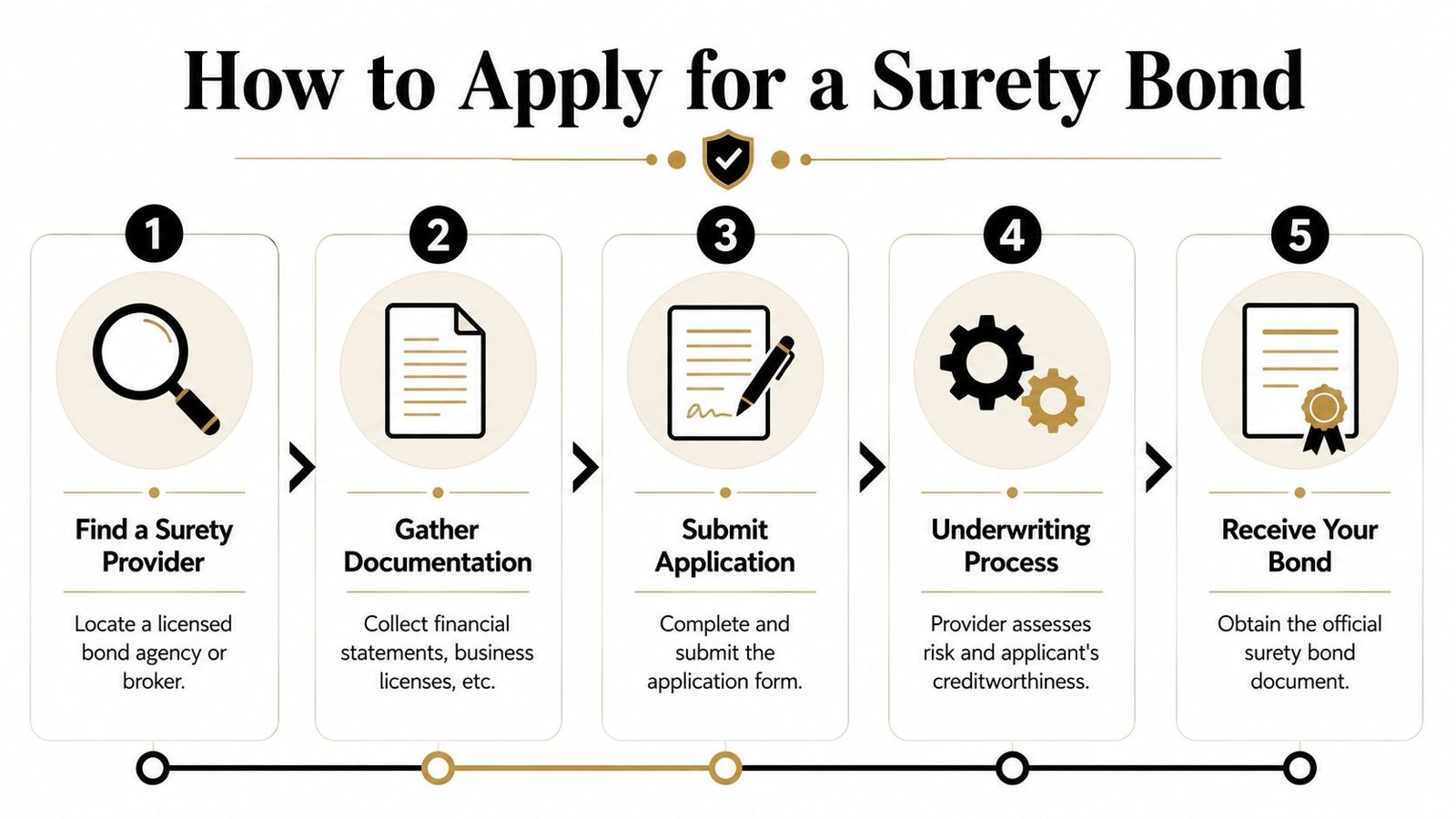

How to Apply for a Surety Bond

The application process feels intimidating until you break it into pieces. Applicants typically don't fail because the form is impossible. They get stuck because they don't know what the underwriter is trying to verify.

The basic workflow

Identify the exact bond requirement

Get the bond name, amount, and obligee exactly right. A “contractor bond” is too vague. You need the specific requirement tied to your license, contract, or court matter.Choose a legitimate surety provider

Work with a licensed agency or broker that regularly handles the bond type you need. A bail-related bond and a contractor compliance bond are not processed the same way.Gather your paperwork

Depending on the bond, this may include business details, license information, financial records, ownership information, and contract details.Submit the application for underwriting

The surety reviews risk. They want to know whether you're likely to fulfill the obligation and whether they'd be comfortable backing you.Pay the premium and file the bond

Once approved, you pay the premium and receive the bond form for filing with the court, agency, or obligee.

A short quote process can help you see what information is usually requested before you commit. This online surety bond quote page is a good example of the kind of basic intake details agencies often ask for.

What underwriters are really looking at

Underwriters aren't trying to make your life harder. They're making a risk decision. They usually care about your credit profile, business history, financial strength, and whether the bond obligation is straightforward or high-risk.

For some bonds, the process can move quickly when your information is complete. For New Jersey freight brokers, federal law requires a $75,000 surety bond. Underwriting is typically completed within 24–48 hours after electronic filing, based on New Jersey freight broker bond guidance.

That speed doesn't happen by magic. It usually happens because the applicant submitted clean information the first time.

Here's a quick walkthrough that helps visualize the process:

How to make the process smoother

- Match names carefully: Your legal business name should match your registration and supporting documents.

- Answer directly: If the application asks about ownership, prior claims, or financial issues, don't hedge.

- Start early: Bonding delays usually happen when someone waits until a renewal or contract deadline is already on top of them.

If you're organized, most of this is routine. If you're rushed, even simple bonding can turn into a scramble.

Typical Surety Bond Costs and Premiums

A common first question is: “What will this cost me?” The honest answer is that the bond amount and the premium you pay are different numbers.

The obligee sets the required bond amount. The surety then prices your premium based on risk. In New Jersey, surety bond premiums typically range from 1% to 10% of the total bond amount according to New Jersey surety bond pricing information. That same source notes that a standard $10,000 NJ Auto Dealer Bond may cost a low-risk applicant with good credit just $100 to $300 annually.

What affects your premium

A surety usually prices around a few practical questions:

- Credit profile: Stronger credit often leads to lower rates.

- Bond type: Simple license bonds are often easier to price than large contract bonds.

- Business history: A stable operating record helps.

- Claim exposure: The more risk the surety sees, the more the rate can rise.

That's why two people applying for the same bond amount may get very different prices.

Example Surety Bond Premiums in New Jersey (2026)

| Bond Amount | Credit Profile | Estimated Premium Rate | Estimated Annual Cost |

|---|---|---|---|

| $10,000 | Good credit, low-risk applicant | 1% to 3% | $100 to $300 |

| $10,000 | Higher-risk applicant | Up to 10% | $100 to $1,000 |

| $75,000 | Good credit freight broker | 1% to 5% | $750 to $3,750 |

| $75,000 | Fair or poor credit freight broker | 5% to 15% | $3,750 to $11,250 |

The freight broker row reflects a separate verified New Jersey-related example. Federal law requires a $75,000 freight broker bond, and annual premiums can range from 1% to 15% of the bond amount depending on credit, as explained in the earlier freight broker source.

Cost check: A cheap premium doesn't mean the obligation is small. It only means the surety thinks the risk of a claim is lower.

People also confuse bond pricing with bail pricing. If you're sorting out that separate question, this plain breakdown of how much a bail bond costs helps keep those categories from getting mixed together.

How to Verify a New Jersey Surety Provider

When money is tight and time is short, people skip verification. That's exactly when mistakes happen. Before you hand over personal information, sign an indemnity agreement, or pay a premium, make sure the provider is real and authorized.

Start with the company's authority

For public work in New Jersey, the state relies on approved sureties. The verified data notes that the New Jersey Department of Banking and Insurance maintains the official list of approved sureties eligible to issue these bonds, as described in the earlier state-project bonding source. That matters because a bond is only useful if the obligee accepts it.

If a company can't clearly explain its authority to issue your bond type, stop there.

Use a practical screening checklist

- Confirm the exact bond type: Ask whether the provider regularly issues that specific New Jersey bond.

- Check the surety company name: Don't rely only on the agency name. The actual surety backing the bond matters.

- Review the paperwork before paying: Make sure the obligee name, bond amount, and principal name match the requirement.

- Read the indemnity section: Personal repayment responsibility is typically found within this section.

- Look for reputation signals: Read independent feedback and complaints, not just marketing copy.

A quick reputation check can save you trouble later. If you want a model for how consumers screen service providers carefully, this guide on reading bond-related online reviews shows the kind of details worth paying attention to.

Watch for red flags

A legitimate provider should be able to answer basic questions without dodging. Be cautious if someone:

- Pushes urgency without clarity

- Won't identify the surety company

- Avoids sending sample paperwork

- Brushes past repayment language

- Uses vague promises instead of specifics

You don't need to become a bond expert overnight. You just need to verify that the company, the form, and the authority all line up before you sign.

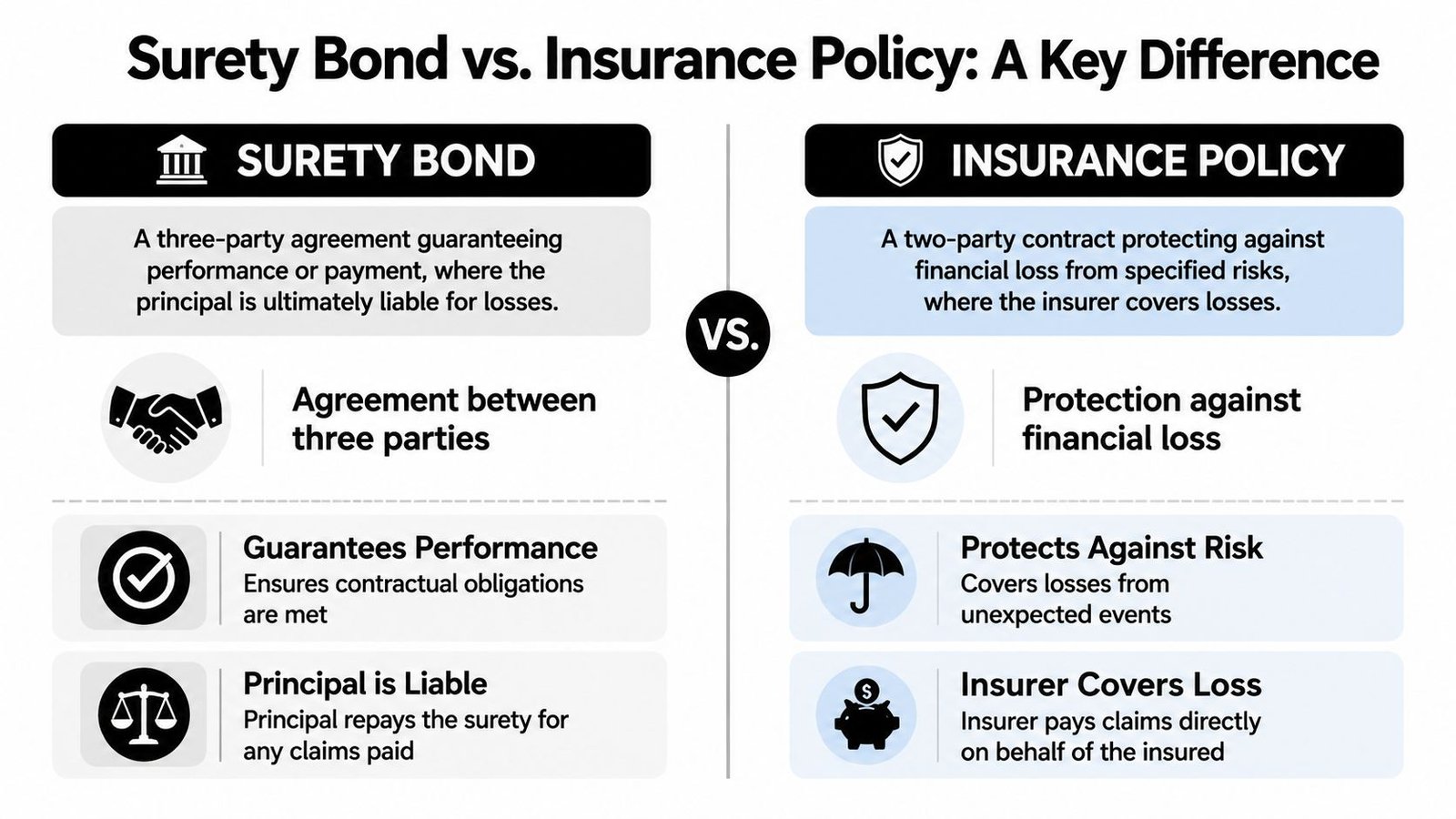

The Critical Detail Most People Miss About Bonds

This is the part people often learn too late. A surety bond is not insurance for the person buying it.

Insurance usually protects the policyholder against a covered loss. A surety bond works differently. It protects the obligee or the public by guaranteeing that the principal will perform, pay, comply, or appear as required.

What happens after a claim

If a valid claim is made and the surety pays, the story doesn't end there. New Jersey law confirms that if a surety pays a claim, the contractor is personally obligated to reimburse the surety in full. This makes the bond a form of credit, not insurance, a detail that 42% of contractors reportedly misunderstand, leading to unexpected financial strain, according to this New Jersey contractor bond explanation.

That one point changes how you should read every bond document. The premium you pay is not buying you claim forgiveness. It's buying the surety's backing, subject to your repayment promise.

Why this surprises people

People hear “coverage” and assume risk transfer. That's not how bonding works for the principal. The surety expects you to stand behind the obligation and to repay losses if the surety has to cover them.

Here's the plainest way to put it:

| Product | Who it primarily protects | If money is paid out |

|---|---|---|

| Insurance policy | The insured party, subject to policy terms | The insurer generally bears the covered loss |

| Surety bond | The obligee or public | The principal may have to reimburse the surety |

Before you sign a bond agreement, read it like a loan guarantee, not like an insurance card.

That's why transparency matters so much. A good bond professional explains repayment risk before the paperwork hits your inbox. If you value that kind of direct communication in high-stress legal situations, you can see how a service-oriented agency presents local help on the Jefferson County Golden Colorado bail bond page. The setting is different, but the communication standard should be the same. Clear, plain, and honest.

The safest mindset

Don't ask only, “Can I get approved?” Also ask, “What obligation am I personally backing?” That one habit can keep a bond from turning into a nasty financial surprise later.

Frequently Asked Questions From Families

What happens if someone misses a court date on a bail bond

The court may treat the bond as in default and start a forfeiture process. That doesn't always mean the worst happens instantly, but it does mean the situation gets serious fast. Families should contact the attorney and the bond agent immediately and start fixing the missed appearance, not waiting to see what happens next.

The biggest mistake is silence. Courts care a lot about whether the person returns and whether the family responds quickly and responsibly.

Do you get the premium back

Usually, no. The premium is the cost of obtaining the bond. It is not the same as a refundable cash deposit posted directly with the court.

That's one reason people need to understand the product before signing. You're paying for the surety's guarantee and the work involved in issuing the bond, not placing money in a savings account that automatically comes back later.

When is collateral required

Collateral may be required when the risk is higher, the bond amount is large, the financial profile is weak, or the facts are unusually uncertain. In bail situations, collateral can also come up if the agent believes the risk of nonappearance is high.

The exact rule varies by bond type and provider. Ask directly whether collateral is required, what form is acceptable, and under what conditions it will be returned.

How is a surety bond different from cash bail

Cash bail usually means the full amount is posted directly with the court by the defendant or family. A surety bond uses a surety company's backing instead. That can reduce the amount needed upfront, but it also creates a separate contract with repayment and compliance obligations.

If your family is choosing between those two options, slow down and compare the tradeoffs. Upfront cost is only one factor. Risk, refundability, timing, and paperwork matter too.

What should families ask before signing anything

Use this short checklist:

- Who is the obligee: Court, agency, or project owner?

- What exactly is being guaranteed: Appearance, payment, performance, or license compliance?

- What is the premium: And is any part refundable?

- Is collateral required: If yes, on what terms?

- Who is personally responsible: The defendant, contractor, business owner, or cosigner?

- What triggers a claim or forfeiture: Missed court date, nonperformance, or a compliance failure?

The right question isn't “How fast can I sign?” It's “What am I agreeing to repay if something goes sideways?”

If you're dealing with a bond issue and need clear answers from a team that handles urgent situations every day, Express Bail Bonds offers straightforward help, fast communication, and practical guidance. Families who need local detention support can also review the Centennial bail bonds page for an example of how the process is explained in plain English before anyone signs paperwork.